Warning: Big Changes Coming to Humana Advantage 2025

This information is for you if you currently have a Humana Medicare Advantage plan.

I want to highlight some of the key points in an article that is currently circulating the internet about Humana’s concerns regarding the 2025-year reimbursement rate and how that affects you as a Medicare Advantage member with Humana.

Update: If you have received notice that your plan is changing or ending, please call us to find an alternate option: 888-414-4547

So within this page, I’ll cover:

- The bad

- The good

- My final thoughts on how you can be prepared

The Bad: Plan Removals

We are jumping right into the bad.

The screenshot below is pulled directly from the article – which is also linked at the bottom of this page.

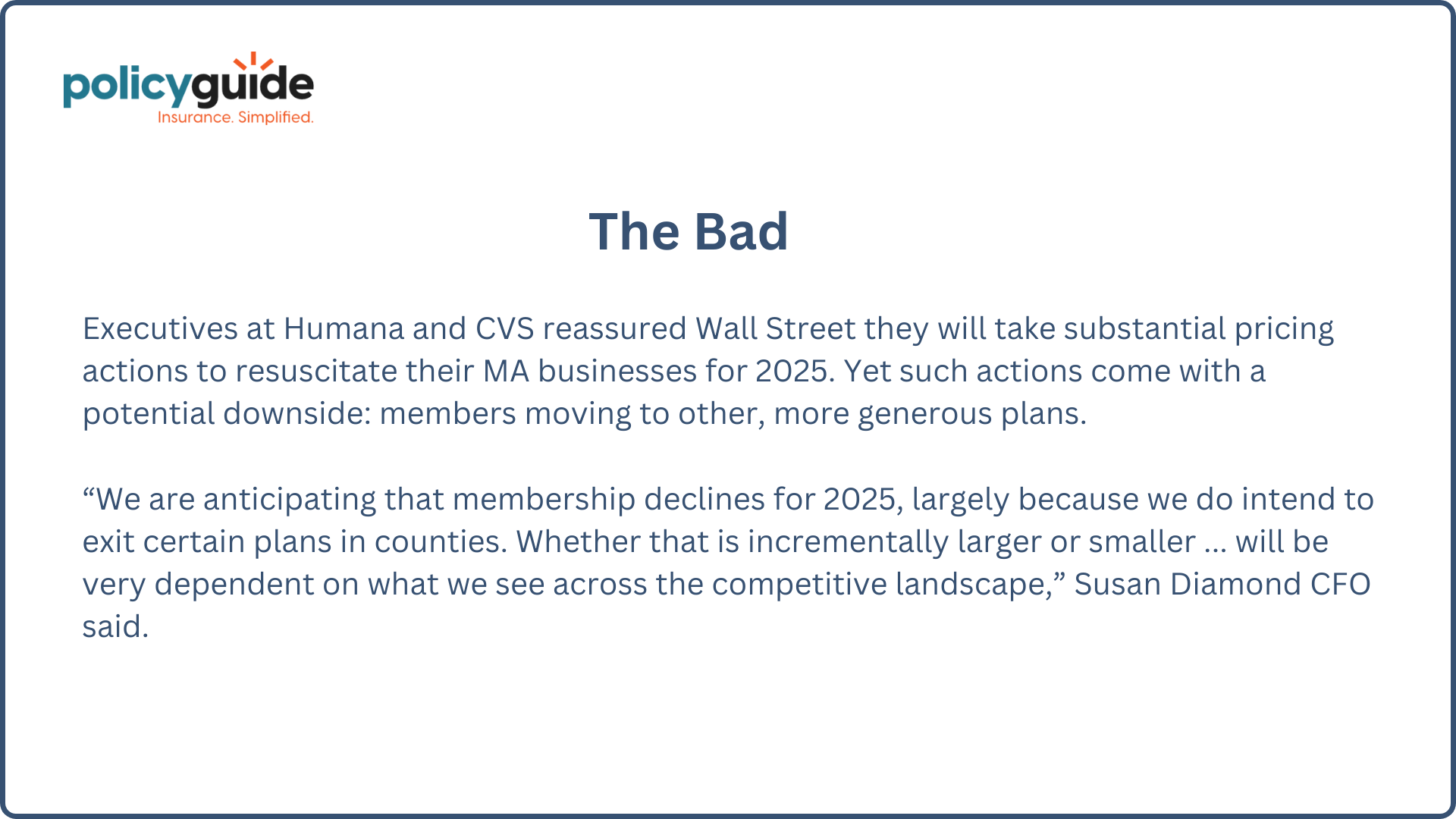

“Executives at Humana and CVS reassured Wall Street that they will take substantial pricing actions to resuscitate their Medicare Advantage business for 2025.”

Resuscitate? That’s not a good word.

“Yet such actions come with a potential downside, losing members or members moving to other, more generous plans.”

And this is a direct quote from Susan Diamond, the CFO at Humana:

“We are anticipating that membership declines for 2025, largely because we intend to exit certain plans in counties. Whether that is incrementally larger or smaller will be very dependent on what we see across the competitive landscape.”

What does that mean? That means that Humana will look at all the counties in the United States. If membership in certain counties is not performing to a standard that they hold for profitability, they may remove those plans from those counties altogether.

So, if you are in one of those countries, that could affect you.

Now, do not panic. This article has been circling around a lot. There’s truth to it, but Humana could make very mild changes you may not experience or are not in a county they leave.

If you are in a county that they leave, you do have guaranteed issue rights to change over to another Medicare Advantage company. You can seamlessly change plans or companies, no health questions asked. So, there are safety mechanisms in place to protect you.

The Bad: Benefit Cancellations

Moving on to discuss how benefits could be affected.

What’s my prediction? Let me break it down for you.

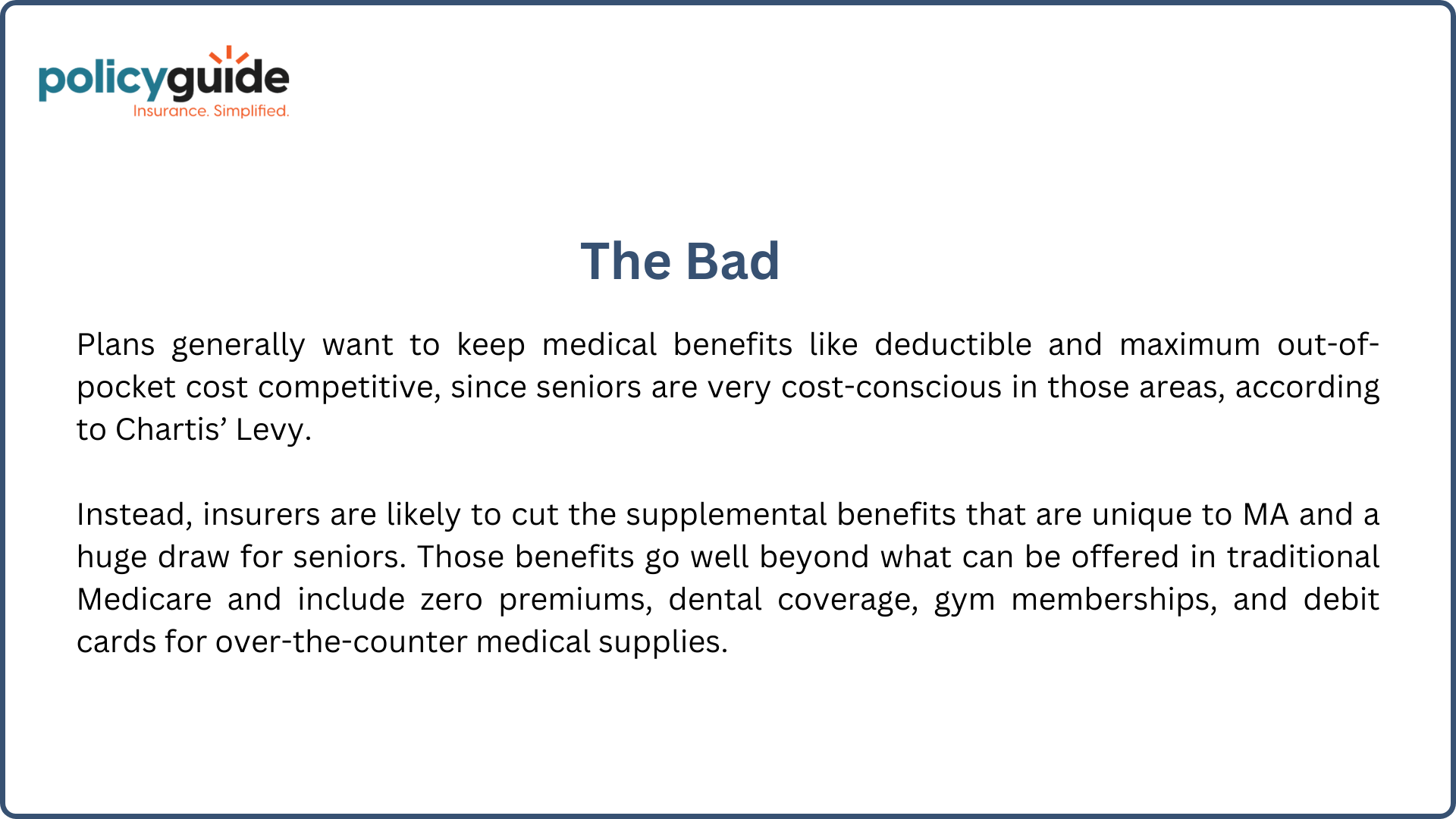

Plans generally want to keep medical benefits (like deductible and maximum out-of-pocket costs) competitive since seniors are very cost-conscious in those areas.

Instead, insurers are likely to cut the supplemental benefits that are unique to Medicare Advantage – and a huge draw for seniors. Those benefits go well beyond what traditional Medicare offers and include zero premiums, dental coverage, gym memberships, and debit cards for over-the-counter medical supplies.

So, that’s my prediction. Having been in the Medicare space for almost 15 years, those things are usually addressed the fastest when profitability is a problem.

They’ll consider questions like:

- The monthly premium. Does that need to be raised?

- Is there a zero premium plan that needs to have a premium now?

- Can they do away with some free ancillary benefits, like dental, vision, gym memberships, or OTC benefits?

You may use these benefits, but if only 20% of the membership is using them, they see it as an opportunity to remove them to cut costs.

The Good: TBC Threshold

Yes, there is good news!

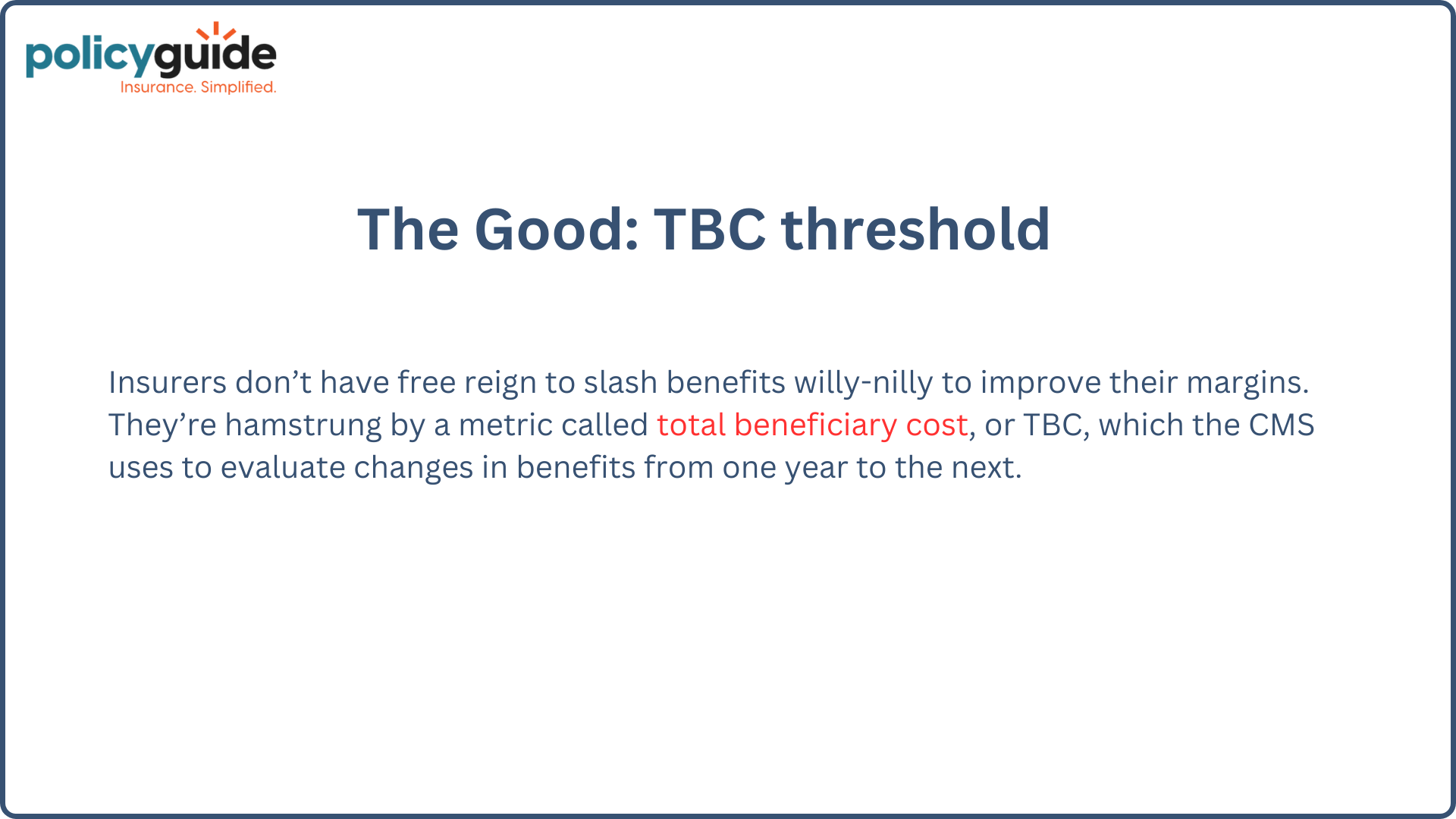

Insurers don’t have free rein to just slash benefits at their will to improve their margins. They’re hamstrung by a metric called Total Beneficiary Cost (TBC) which CMS uses to evaluate changes in benefits from one year to the next.

So, what does that mean?

That means if Humana or any company is having that much trouble, they can’t just go in and start cutting benefits and raising premiums. They’re held to a very strict metric that Medicare has them under.

That’s a huge advantage for the member in terms of protection. It will reduce or curtail major changes.

My Final Thoughts

First, don’t panic. The Medicare Advantage market has its highs and lows, and you will probably see some degree of change.

But here is my advice – the Annual Election Period starts October 15th, and before then, you should:

- Have a list of your medical providers ready

- Have a list of your prescription medications ready

- Have your benefits available so that if you have to make a change, you can look at your Humana copays and find another company, like Aetna or United Healthcare, that offers similar benefits and costs while still covering your current medical providers and prescriptions

This year may be a little bit different with some of these changes. A lot of companies are coming out and saying that the amount CMS is reimbursing for 2025 is not sufficient to keep up with medical costs.

Be a little more diligent this year about checking your plan, benefits, and provider directory and ensuring there are no unforeseeable changes that require you to pick another plan.

I hope this article was helpful to you. Feel free to let us know if there’s anything we can do. Take care.

Source: Humana 2025 Article