Medicare Supplement Plan G: Benefits - Cost Overview

In this article, I’m going to give you five reasons why Medicare Supplement Plan G is my favorite plan.

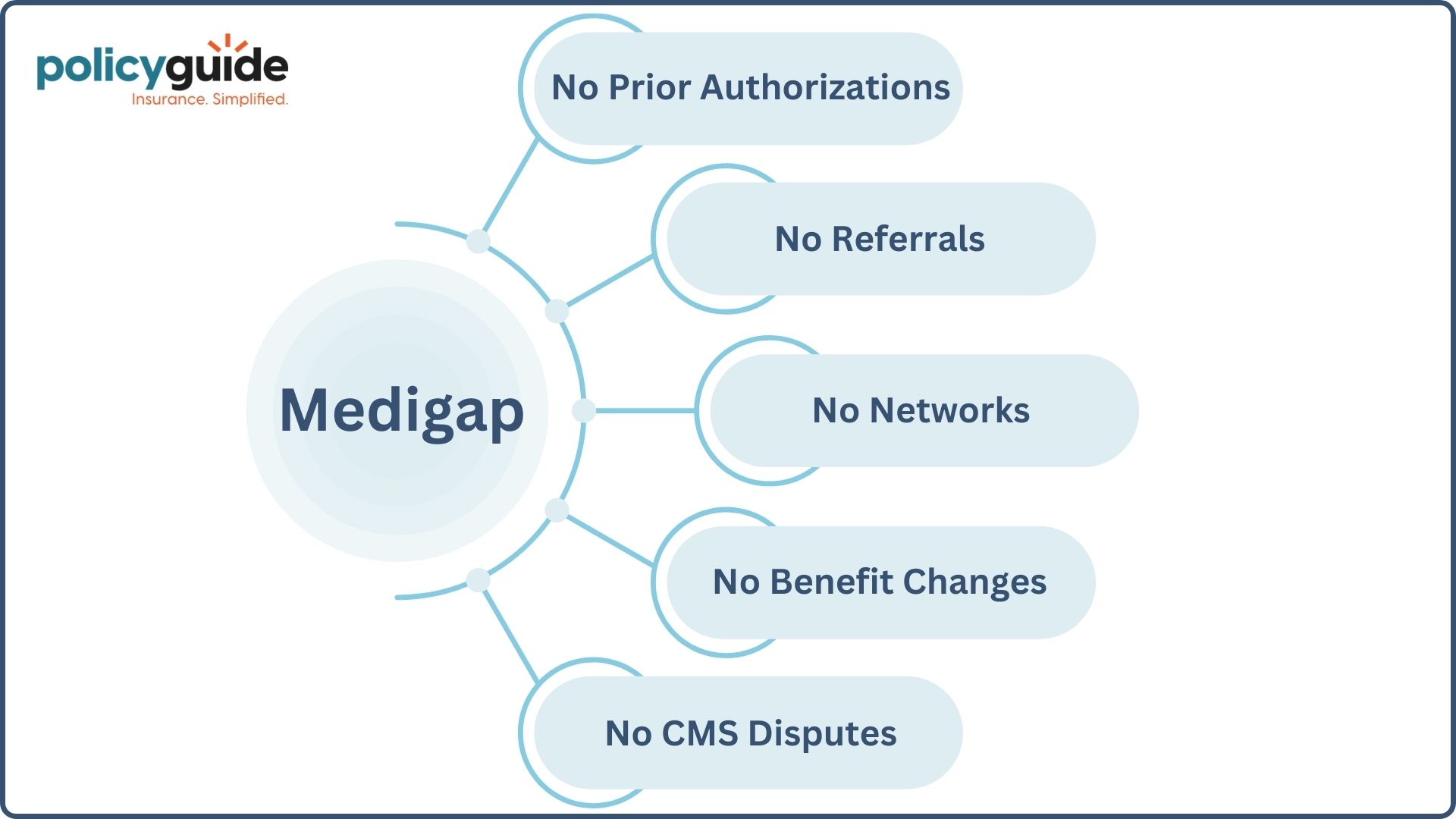

- #1. No prior authorizations

- #2. No referrals

- #3. No networks

- #4. No benefit changes

- #5. No disputes with CMS or the federal government

I’ll break down what these five things mean and how they affect you as a Medicare beneficiary.

I’m Mark Prip. I’ve been a licensed agent since 2003, exclusively working with folks to select the right Medicare plan. I want to give you some highlights and reviews on Medicare Supplement Plan G – and why I think it is one of the best plans.

Talking points:

I’ll discuss coverage, cost, Plan G vs. Plan N, and Plan G vs. a Medicare Advantage plan.

I’ll also provide review data on customer satisfaction for those currently on Plan G.

Let’s jump right in.

Medigap Plan G Overview

Plan G offers extensive coverage and the freedom to choose any network provider. Plan G is the most popular Medigap plan today, with over 3.5 million people enrolled.

One key feature of Plan G is that its benefits are consistent year after year. Plan G is standardized, which means any insurance company offering it is required to offer the same Plan G benefits.

There are no network limitations or referrals, and it boasts lower premiums than Plan F. It’s offered by over 90% of Medigap providers in the country. Your Plan G policy is guaranteed for life as long as you pay your premiums on time.

Benefits of Medicare Supplement Plan G

Let’s look at the benefits and see what this plan entails in terms of your responsibility vs. the cost covered by Original Medicare.

Right out of the gate, you, as the member, experience a $0 copay for anything associated with Medicare Part A. When it comes to Medicare Part B, it covers 100% after you pay a $257 annual deductible.

Coverage includes:

- Outpatient testing

- Doctor office visits

- Part A hospice care coinsurance (or copayment)

- Hospitalization

- Skilled nursing facility care for up to the first 100 days

- An extra 365 days of hospital care after the Original Medicare lifetime reserves have been used

There is also a foreign travel emergency benefit. Beneficiaries receive 80% coverage for emergency care outside of the United States or its territories. Plan G has a lifetime maximum of $50,000 for foreign travel emergency care after a $257 deductible.

What Is The Out-of-Pocket Maximum for Medigap Plan G?

While there’s no official out-of-pocket maximum, your expenses with Medigap Plan G are quite predictable. Here’s what you can expect to pay:

- Medicare Part B Deductible: The only cost you must cover before Plan G starts paying is the annual Medicare Part B deductible ($257 in 2025). Once you’ve paid this, Plan G covers 100% of your Medicare-approved expenses.

- Non-Medicare Covered Services: Medigap Plan G does not cover dental, vision, hearing, or prescription drugs, so any costs for these services would be paid out of pocket unless you have additional coverage.

Why the Lack of an Out-of-Pocket Maximum Isn’t a Concern

Even though Medigap Plan G does not have a formal out-of-pocket maximum, it provides nearly full coverage after you meet the Part B deductible. This differs from Medicare Advantage plans, which often have higher cost-sharing and a maximum cap on out-of-pocket spending.

With Plan G, the worst-case scenario in a given year typically involves the Medicare Part B deductible and any potential excess charges, making it a very financially predictable option.

How Much Does Medigap Plan G Cost?

In 2025, the average monthly cost of Plan G is between $110 and $180. However, the monthly premium for Plan G can vary depending on your state, age, gender, and tobacco use.

Medicare Plan G Rate Comparison: Cigna, Mutual of Omaha, Aflac, and Aetna

When selecting a Medicare Supplement Plan G, it’s important to understand that the benefits are standardized across all insurance providers. This means that no matter which company you choose, the core coverage remains the same.

However, what does vary are the monthly premiums, available discounts, and additional perks that some providers offer.

Below I will compare Plan G rates from leading providers. The key factors to consider when choosing a provider include:

- Monthly Premiums – Prices differ based on factors like age, location, and provider.

- Discounts & Savings – Some insurers offer household or multi-policy discounts to help reduce costs.

- Extra Benefits – Some providers include additional perks such as dental, vision, or hearing coverage.

- Company Reputation & Financial Strength – A reliable company ensures peace of mind and smooth claim processing.

To help you make an informed decision, the following chart compares the monthly premiums for each provider.

| Medigap Provider | Alabama | Georgia | Texas | Florida | Pennsylvania |

| Cigna | $160.41 | $170.03 | $132.64 | $190.13 | $151.86 |

| Mutual of Omaha | $198.57 | $202.73 | $158.70 | $227.25 | $186.36 |

| Aflac | $159.84 | $200.83 | $149.37 | $228.20 | $154.29 |

| Aetna | $206.33 | $199.09 | $200.25 | $258.48 | $178.85 |

| Plan G sample quotes are for a 65 y/o nonsmoking male. |

|||||

What Does Plan G Not Cover?

As I mentioned before, Plan G does not cover the Part B deductible. You’ll be responsible for the first $257 of outpatient care per calendar year. Plan G will cover Part B excess charges.

It does not cover pharmacy or RX benefits, so you would need to consider enrolling in a separate prescription drug (Part D) plan.

Is Medicare Plan G Accepted Everywhere?

Yes, Medicare Supplement Plan G is accepted everywhere that Original Medicare is accepted.

Here’s how it works:

- Medicare Supplement (Medigap) Plan G is not a network-based plan, meaning you can visit any doctor, hospital, or provider in the U.S. that accepts Medicare.

- Because Original Medicare (Part A & Part B) is your primary insurance, Plan G works as secondary coverage, paying after Medicare covers its share.

- There are no network restrictions, no referrals needed, and you can use it in all 50 states.

Important Notes:

- Foreign Travel: Plan G covers 80% of emergency medical care outside the U.S. (after a $250 deductible, up to a $50,000 lifetime limit).

- Medicare Assignment: As long as a provider accepts Medicare assignment, Plan G will pay as expected. However, if a provider does not accept Medicare, you may have to pay excess charges (which Plan G covers in most cases).

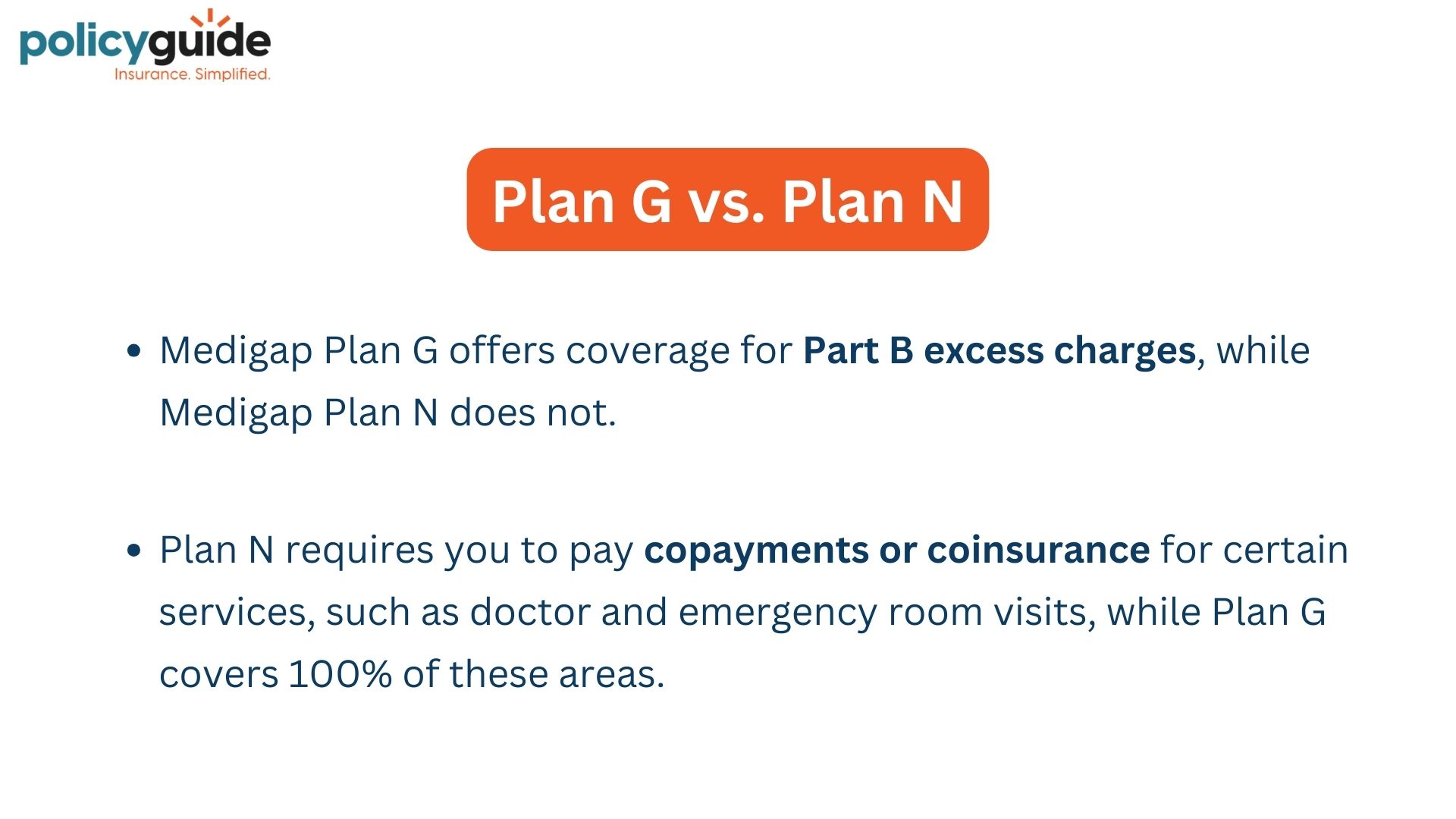

Plan G vs. Plan N

Plan N is definitely the second most popular plan compared to Plan G, so they are very similar.

Medigap Plan G offers coverage for Part B excess charges, while Medigap Plan N does not. Plan N requires you to pay copays or coinsurance for certain services, such as doctor and emergency room visits, while Plan G covers 100% of these areas.

So let me jump back to the excess charges. That means that a doctor is allowed to charge upwards of 15% above the Medicare allowance. When you’re on Plan G, it will pay that for you.

If you’re on Plan N, those excess charges for Part B would not be covered. Those would be your responsibility.

Plan G vs. Medicare Advantage

This is probably the most important part of this page that I want you to pay really close attention to because, as I’m sure you’re fully aware, the two most common avenues for folks on Medicare are a Medicare Supplement (usually Plan G) or a Medicare Advantage plan. The two operate very, very differently.

So let’s start with Medigap.

Probably the single most important factor is that Medigap Plan G does not require prior authorizations.

-

Prior Authorizations

- When you’re taken to the hospital, a prior authorization means the insurance company has to be notified about the recommended procedure by the facility, doctor, or hospital. The Medicare Advantage company can then deny or approve that prior authorization request.

I’ll point out that in a 2021 Kaiser Family Foundation study, over 35 million Medicare Advantage prior authorization requests were processed, and over 11 million were denied.

Consider it this way:

- You’re experiencing chest pain. You go to the emergency room. They’re going to run you through a stress test, some lab work, and then maybe do a heart catheterization.

- For every one of those steps, the Medicare Advantage plan could require prior authorization, meaning they won’t go through with the procedure until that prior authorization is approved – it could be minutes, hours or days.

- Medigap plans (no matter which Medigap plan you have) have no prior authorizations. That means your care can continue quickly, without any middlemen deciding whether that procedure is approved or not.

The next big thing is Medigap Plan G does not require referrals.

You do not have referrals, nor do you have to work inside of networks like an HMO or a PPO. You have the freedom to go wherever you want. As long as Original Medicare is accepted, any Medicare Supplement plan, including Plan G, is then automatically accepted by that provider.

No benefit changes. With Medicare Advantage plans, there’s potential that those change every calendar year. Maybe your copays will go up. Maybe your pharmacy list changes. Maybe your premium goes up, or maybe you had a plan without a premium, and now it has a premium.

-

Important:

Medicare Advantage has a greater potential for plan and benefit changes. Once enrolled in Medigap Plan G – whatever your benefits are – they’re locked in and stay the same year after year.

And last on my list is no CMS disputes.

Because CMS, or the federal government, goes into a contract with a Medicare Advantage company, every year, CMS decides how much they’re going to reimburse a Medicare Advantage plan company for your enrollment.

So, over the years, that amount could be favorable. Insurance companies are grateful, and they don’t change anything. That amount can come down in other years, and CMS offers a lower reimbursement rate. That Medicare Advantage plan will now be pressed to figure out how to remain profitable, so they may squeeze your benefits, remove medications from the RX list, or change the network.

- If CMS does not increase the reimbursement to that company, the company’s only option is to reduce its benefits or change the network to offset the amount the federal government is not paying.

There are many ways to rein in the cost of Medicare Advantage, so when I say no CMS disputes, that’s the beauty of Medigap Plan G. There are no reimbursement rates. There’s no negotiating. It’s very simple, very black-and-white.

Original Medicare pays its bulk, which is generally 80% of the claims. Medigap plan G comes in and pays the difference. There’s no money being exchanged from a Medigap company and CMS about enrollment. You simply pay your Original Medicare A and B cost, and your Medigap premium. There’s no in-between reimbursement between the two.

How Do I Enroll in Medicare Supplement Plan G?

Enrolling in Medicare Supplement Plan G is a straightforward process, but it’s important to choose the right plan and company to fit your specific needs. Here’s a step-by-step guide on how we help you navigate this process seamlessly.

Step 1: Fact-Finding – Determining the Best Plan for You

Before enrolling in Plan G, we start by gathering essential information to ensure you get the best possible coverage and pricing.

This includes:

- Your Date of Birth (DOB) – Determines eligibility and potential rate adjustments.

- Smoker Status – Tobacco use can impact your premium rates.

- Marital Status & Household Discounts – Some insurance companies offer discounts if a spouse or household member also has a Medigap policy.

- Location – Medicare Supplement Plan G rates vary by state and zip code.

- Current Health Conditions – Helps determine if medical underwriting will be required.

Step 2: Comparing Plans and Finding the Best Rate

Once we have your details, we compare top-rated insurance companies offering Plan G in your area.

Since benefits are standardized, our focus is on:

- Monthly Premium Costs – Ensuring you get the most competitive rate.

- Company Stability & Reputation – Selecting a financially strong and reputable provider.

- Rate Increase History – Looking at past trends to estimate future premium changes.

Step 3: Completing the Enrollment Process

After selecting the best Medicare Supplement Plan G provider, we make the enrollment process simple and hassle-free:

- We assist you in completing the application right over the phone in just minutes.

- Most applicants receive their policy approval and ID cards within 7-10 days.

- Our team handles everything for you—from application submission to follow-ups.

Why Choose Us?

With over 15 years of Medicare experience, we make sure you get expert guidance, unbiased plan comparisons, and personalized service at no cost to you.

Customer Plan G Reviews

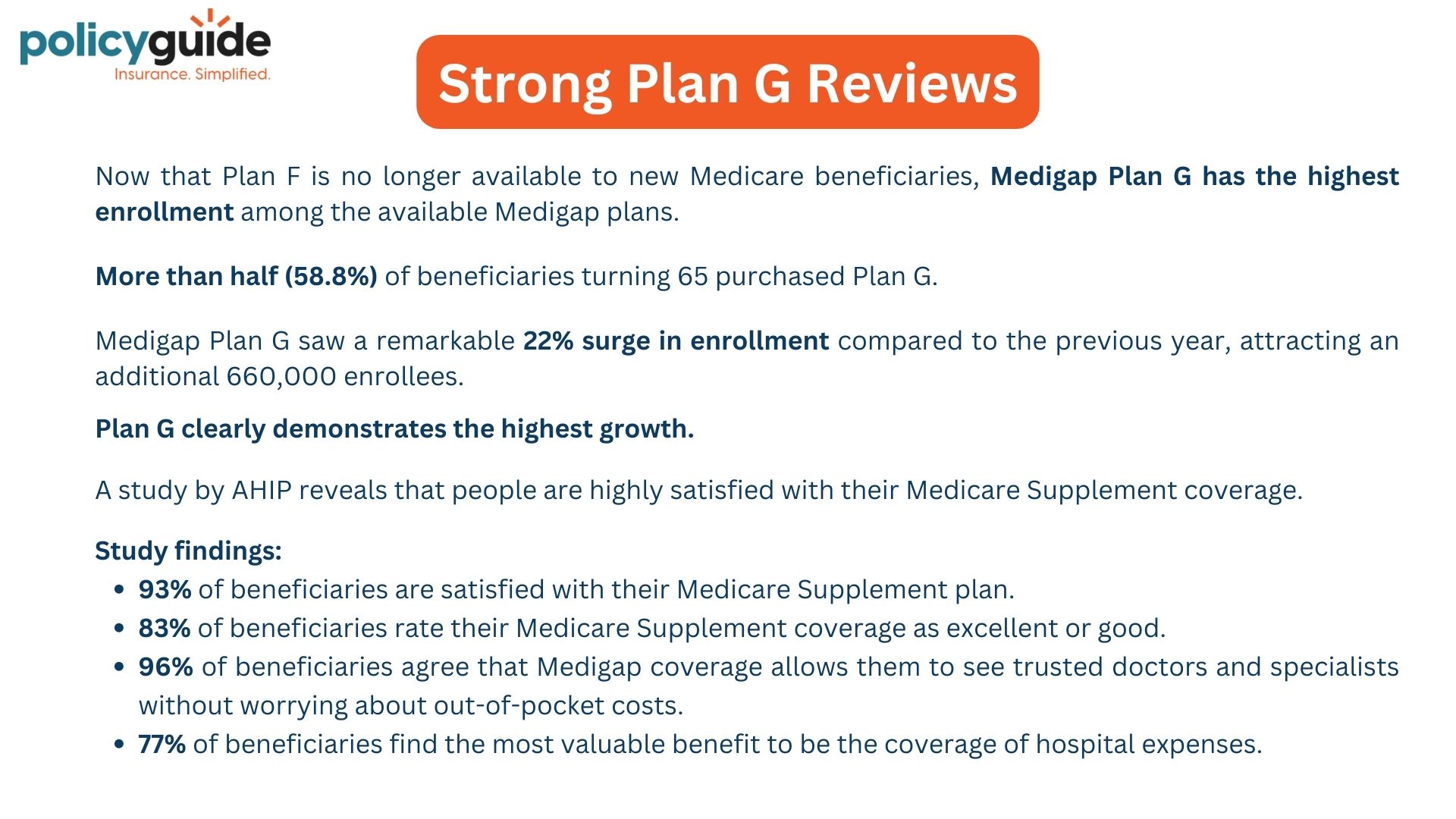

I wanted to point out the strong Plan G reviews. Now that Plan F is no longer available to new Medicare beneficiaries, Medigap Plan G has the highest enrollment among every available Medigap plan. More than half, 58%, of beneficiaries turning 65 purchased Plan G.

Medicare Plan G saw a remarkable 22% surge in enrollment compared to the previous year, attracting an additional 660,000 enrollees. Plan G clearly demonstrates the highest growth rate.

A study performed by AHIP revealed that people are satisfied with their Medicare Supplement coverage. The findings were this:

- 93% of beneficiaries are satisfied with their Medicare Supplement.

- 83% call their coverage good or excellent.

- 96% agree that Medigap coverage allows them to see trusted providers and specialists without worrying about out-of-pocket costs.

- 77% of beneficiaries find the most valuable benefit to be the coverage of hospital expenses.

Final Thoughts

My biggest thought on this is that with Medicare Advantage, the big print gives, and the fine print takes away.

And what I mean by that is, from the surface, a Medicare Advantage plan is very appealing because roughly 77% of Medicare Advantage plans have a $0 monthly premium. That’s very appealing to a lot of people.

BUT – then you have copays for all the various services. You may pay $20 for a doctor. You may pay $70 for a specialist. You may pay $400 a day per hospital stay per day. So, if you’re going in for three days at $400, that $1,200 adds up pretty quickly.

With Medigap Plan G, you start with a higher monthly premium. There are no copays. Medigap Plan G pays for any deductibles that Original Medicare has outside of your Part B deductible, which is very small— only $240 per year.

No network changes, referrals, or disputes between a provider and the insurance company or CMS.

If you can afford Medigap Plan G, I highly recommend it. If you have questions about either one, email or give us a call. Our job is to try to make the Medicare road easier because, as I’m sure you’ve seen, it’s very complicated.

Kaiser Family Foundation | AHIP Research | AHIP Trends

FAQs

- Which Medicare Supplement plan has the highest level of coverage?

- What are the best Medicare Supplement providers?

- When am I eligible for Medicare coverage?